There is an elephant in the room. Jim Rickards has been making some bold predictions while on his book tour for Currency Wars. He says that in the case of a collapse of confidence in the dollar, the U.S. could confiscate the gold owned by foreign governments, Germany in particular, that is stored in NYC at the Fed. He says the U.S. could then use this gold to dictate a new international monetary system based on U.S. currency, just like last time.

Here are a couple of Jim's tweets on the subject:

@JamesGRickardsGot a bid from #Germany for foreign rights to #CurrencyWars. Germans should read it. Ch. 11 tells why they'll never see their gold again

@JamesGRickards@FrankfurtFinanz Yes. This is described in Ch 5 and Ch 11 of #CurrencyWars. #Germany will never see its #gold again

We don't like to ignore elephants at FOFOA, so please discuss. Should those countries with gold stored at the Fed be worried? I just know this makes different people uncomfortable for different reasons. I posted some of my own thoughts here in response to Wandee who wrote, "I’m hoping Rickards is right per Blondie’s post above and the US/West can muster up 20ktons and figure out some kind of new currency alignment."

Also, Jim was interviewed by Eric King at KWN the other day. Here's the link. And here's a partial transcript (h/t Blondie):

“...I can see it happening, and it might even be a good thing in the sense that if we combined the official US gold of 8000 tonnes and I think 6000 tonnes that we could confiscate from the Europeans, Japanese and the IMF, and there’s another several thousand tonnes out at JFK airport in warehouses controlled by ScotiaBank and HSBC, its amazing how concentrated the gold is, its not in that many places, its really ten, you can count ten places that hold really the vast majority of all the official gold in the world, combine all that gold and the US could easily have 17,000 tonnes or upwards of 20,000 tonnes, which is you know 70% of all the official gold in the world. That’s enough to dictate the outcome of the international monetary system. It would be like, it would be a lot like Bretton Woods... [other nations] they might as well have stayed at home because the US dictated the outcome... We could do it again if we had that much gold, we could say hey, here’s the deal, here’s the new currency, its the new American dollar, backed by gold, all you other people have to peg to it and if you want your gold back, get to work, and, and try earning it and you know we’ll give you an IOU or something.

Again, this is an extreme scenario, but I think it is something that would be likely to happen in extreme distress. I mean, governments are not just going to throw up their hands, if we have some kind of collapse of confidence in the dollar the United States government is not going to curl up in a ball and cry, they’re going to use executive orders and executive power to dictate an outcome.

[comparing the US to Rome as the current world superpower]... if we converted the European gold for our own purposes, think of it as a 100% tax”

Rickards on the euro! Here's Jim from this morning on CNBC Worldwide Exchange. He's great on the euro and gold, as long as he refrains from predicting a confiscation of custodial gold, a 90% tax on old gold and a new U.S.-led gold price fixing scheme.

FOA on currency war: We will see the beginnings of a currency war like no other in our time...

Several years ago, many gold bugs and gold advocates missed the path as the trail turned. Something I pointed out at the beginning of these "message" talks. As most of you will no doubt agree, almost all gold discussion still centers around "the dollar's war with gold". Truly, the evolution of this story will be how that war ended then and now the dollar's war with the Euro began! A very large part of that war strategy, employed by the ECB/BIS, was to let the dollar / IMF faction hang themselves by expanding and supporting the whole arena of this dollar paper gold market. Inflating the gold market place with so much "paper gold" that we would eventually have to bankrupt ourselves just to keep the dollar in the war game against the Euro.

Yes, the war now is between the Euro and the dollar! The Washington Agreement placed gold "on the road to high prices" as it signaled a phasing out of Euro support for our American gold values. How fast gold can, now, rise will gauge how much staying power the dollar has in all this. If there is any gold war now, it's to be in just how fast the dollar gold market can disintegrate into worthless IOUs! So, don't count on this destruction of our paper gold market to mark the real value and availability of physical gold; that ratio will split somewhere down the goldtrail. This action will scare most harden gold investors to death; especially the ones in leveraged gold stocks and lesser white metals!

The war between gold and the dollar has been over for a while now. The action, today, is between the dollar and the euro arena and this is what will break the price lock on gold. Leaving gold bugs with a lot of questions that ask why this: both systems will strive for a higher currency price for gold; one doing it because they have to; the other doing it because they want to! The casualty on this battlefield will be the world gold market as we know it. A market caught between how Western perception thinks gold's price should be "discovered" and at what price level trading in physical gold craters the entire paper structure. A structure of American based "paper gold".

We have been saying for some time that this will be "the" show to watch unfold; but only if your holdings allow you to stay still in your seat as it happens (smile).

They shifted their war on gold to become a war on the Euro,,,, only too late. Now, knowing that the Euro is a fact, we must have a super gold price if the dollar is to stay in the game! The question becomes one of supporting a cheap paper price for the sole function of keeping the market and all its bullion players alive. With the war on gold over, they need to turn their tanks around to face the real enemy but cannot.

FOA (10/3/01; 10:21:26MT - usagold.com msg#110)

Now that the Euro block is passing a point where the Euro currency is viable; this same past dollar support that built American's illusion wealth will now fall away. In its place we will see the beginnings of a currency war like no other in our time.

Have you ever wondered what money really is? You'll notice that everyone you read has a strong opinion about what money actually is, but who's right? Is money really just one single thing and then everything else has varying levels of moneyness relative to real money?

Is gold real money? Or is money whatever the government says it is? Or is it whatever the market says it is? Is silver money in any way today? Are US Treasury bonds money? Is real money just the monetary base? Or is it all the credit that refers back to that base for value? Is money supposed to be something tangible, or is it simply a common unit we use to express the relative value of things?

Is money really the actual medium of exchange we use in trade? Or is it the unit of account the various media of exchange (checks, credit cards, PayPal) reference for value? Should the reference point unit itself ever be the medium of exchange? Some of the time? All of the time? Never? Is money a store of value? And if so, for how long? Is money supposed to be the fixed reference point (the benchmark) for changes in the value of everything else? Or is it simply a shared language for expressing those changes?

So many questions, right? And how often have you seen these questions even asked, let alone answered? Is money something that changes over time? Or is money's true essence the same concept that first emerged thousands of years ago? And probably the most important question: Does the correct view of money produce answers that are vastly superior to the blind conjecture prescribed by all other views?

Answers

I wonder if it's even possible to answer all these questions in one post. It's a neat challenge in any case, isn't it? As I said at the top, everyone has a strong opinion about what money actually is. So "everyone" will probably disagree with what I write. But that doesn't mean they are right and I am wrong. I want to challenge you to use your own mind and see for yourself. Take what I say and then take what they say, compare, contrast, analyze and then decide for yourself. The prescription produced by my view is quite simple. And only you can decide if it is vastly superior to their blind conjecture.

The Pure Concept of Money

According to Webster's the word 'money' emerged in the English language sometime during the Medieval period in Europe, maybe around the late 1200s. Wikipedia suggests a possible etymology originating with the Greek word for 'unique' or 'unit'. The Western term for physical coins that emerged sometime around the late 1500s was 'specie' from the Latin phrase for "in kind" or "payment in kind," meaning "payment in the actual or real form." The word 'currency' came a little later from the Latin word for current or flow, and was married to the money concept in 1699 by the philosopher John Locke who described the "circulation of money" as a flow or current of monetary payments made in specie.

Etymology is important, because with money or "the moneyness of things" we are talking about a vital concept that predates the word by thousands of years. And it's only by understanding the pure concept that we can see the ways the word has been bastardized by the two camps over centuries. The meaning we commonly assign to words may change over time, but that never changes the original concept underlying the emergence of the word in the first place.

Case in point: Is 'money' equal to 'wealth'? Is "gathering wealth" the same as "gathering money?" In the 1950s a Seattle engineer named Howard Long was deeply distressed that his beloved King James Version of the Bible just didn't seem to connect with people when sharing the Word of God. Long felt he needed a new translation that captured the truths he loved in the language that his contemporaries spoke.

It took a couple of decades, but Long's passion became the New International Version (NIV), a completely original translation from Hebrew, Aramaic, and Greek texts that was finally released in 1978. The King James Version had been translated into English and released 367 years earlier, in 1611. Here is one verse as it appears in each version:

Proverbs 13:11 (KJV) Wealth gotten by vanity shall be diminished: but he that gathereth by labour shall increase.

Proverbs 13:11 (NIV) Dishonest money dwindles away, but whoever gathers money little by little makes it grow.

I use this only as an example of how we sometimes change words to fit our modern understanding, not as any kind of a criticism of the NIV. To be fair, there are many more verses where the NIV does not remove or replace the word 'wealth'. Here are a few other translations of the same verse, which I think will help to illustrate my point about words and concepts:

Proverbs 13:11 (English Standard Version 2001) Wealth gained hastily [or by fraud] will dwindle, but whoever gathers little by little will increase it.

Proverbs 13:11 (Wycliffe Bible 1395) Hasted chattel, that is, gotten hastily, shall be made less; but that which is gathered little and little with hand, shall be multiplied.

Proverbs 13:11 (Young's Literal Translation 1862) Wealth from vanity becometh little, And whoso is gathering by the hand becometh great.

And, just for fun:

"Think now, if you are a person of "great worth" is it not better to acquire gold over years, at better prices? If you are one of "small worth", can you not follow in the footsteps of giants? I tell you, it is an easy path to follow!" --ANOTHER (THOUGHTS!) 1/10/98

The point is, your modern understanding of 'money', and the pure concept of money that emerged long before the word, may be substantially different things. I'll go even further to say that the modern understanding of money is so confused and disputed by the two opposing money camps that the only way we can hope to have a clear view of what is actually happening today is by reverting our understanding to the original concept, before it was corrupted by the two camps.

So now let's go back to the etymology at the top of this section because, while it does not set the pure concept, it does reflect it from a time more proximate and a meaning less corrupted than now. And I should note that etymology is a somewhat subjective and inexact science, kind of like interpreting what you find at an archeological site. So I'm using it only as a tool that helps me share with you a concept, not as proof of the correctness of my concept. There is no proof at this time. There is only the use of your own discerning mind.

If we look at the specific etymology I highlighted, we are pretty close to the pure concept which I will confirm from a couple different angles. 'Money' is a "unique unit" that we use as a kind of language for expressing the relative value of things other than money. The modern example would be "dollar". Not "a dollar," not a physical dollar, but the word "dollar" as it is used to say a can of peas costs a dollar, or my house is worth 100,000 dollars, or you owe me a hundred dollars. If you give me two grams of gold you won't owe me a hundred dollars anymore. You don't have to give me actual dollars. That's just the unit I used to express the amount of value you owed me. That's the pure concept of money.

This is where it gets a little tricky and mind-bending. The actual physical dollar, that physical item we call "a dollar," is not money in and of itself. In other words, it is not intrinsically "money". It is only money because we reference it when expressing the relative value of goods, services and credit. If we stopped referring to it, it would cease to be money even though it would still be a dollar. Can you see the difference? Like I said, it's tricky.

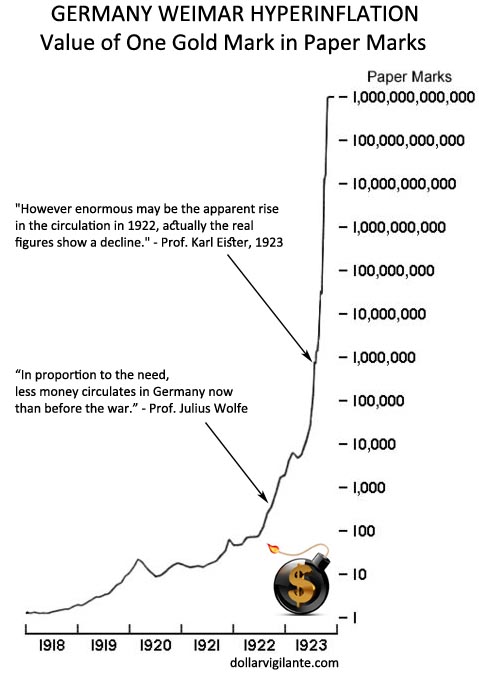

A dollar is just a thing, a tradable item. And it will continue being that same thing even if we stop referring to it when expressing relative values. It will still be a dollar, it just won't be money anymore. Therefore it is not money in and of itself. It is just a thing. Take the old German Reichsbank marks from 1923. Some of them still exist. They are still marks with lots of zeros. But they are no longer money. We can still trade them. I might trade you a few Zimbabwe notes for an original mark, but that obviously doesn't make them money. The same goes for gold. Gold is just a tradable item.

We could be using seashells as money. If we were, then all the seashells available for trade would be the monetary base. That's the base to which I would be referring when I said you owed me one hundred seashells. A single seashell would be the reference point, the unique unit, but the whole of all available seashells would be the base around which money flowed. You could pay your debt to me with either an item that I desired with a value expressed as 100 seashells, or with 100 actual seashells. So if the total amount of seashells available (the monetary base) suddenly doubled making them easier for you to come by, I'd be kinda screwed. Of course I'd only be screwed if the doubling happened unexpectedly between the time I lent you the value of 100 seashells and the time you paid me back.

Getting back to our etymology, the concept behind the term 'specie' meant actual units of the monetary base. In the 1500s, that was the total of all metal coins-of-the-realm available for trade. That was the monetary base of the day and the term 'specie' arose as a way to express payment in the monetary unit itself rather than payment in bulls, or hats, or anything else. But original concept aside, the meaning of the word became married to coins and stuck to this day:

Specie: 1610s, "coin, money in the form of coins" (as opposed to paper money or bullion), from phrase in specie "in the real or actual form" (1550s), from L. in specie "in kind," ablative of species "kind, form, sort"

Notice it says "coins… as opposed to… bullion." That's because while gold coins were referenced in the use of money at the time the word 'specie' emerged, gold bullion was not. "Gold" was not money in and of itself. It was just a thing; a tradable, barterable item. Notice also that it says "money in the form of coins." The coins themselves were also not money in and of themselves. They were only called money because, in that coin form, they were the monetary base that was referenced when expressing the relative value of everything else at that time. Some of those gold coins from the 1500s and 1600s still exist today. Today they are not money, but they are still gold coins. Can you see the difference yet?

Now remember, there's no right or wrong at this point. There's only the usefulness of a perspective in delivering the correct analysis of what's actually happening today and the best prescription for your personal action. But you can't use a perspective until you get it. Then, and only then, you can use your own mind to decide if it is the correct perspective and then act upon it. Later it will be proved correct or incorrect, just as Another said: "time will prove all things."

But in support of this particular view of the money concept, I'd like to direct your attention to Gold Trail Three where FOA went to great length explaining the historical precedents for this view found in the archeological record. Some of this history has been rewritten in hard money text books to fit the modern meaning of words, while the actual historical record—and FOA—tell a different story about the underlying concepts.

Beginning on the third page of The Gold Trail, FOA presents a number of cases in which the hard money camp has corrupted the interpretation of money-related archeological finds in order to make them fit a modern agenda. By projecting modern biases on antiquity, this camp leaves us with estimates of the volume, value and role of ancient gold that may be entirely wrong.

FOA explains "his group's" contentions along with the archeology and sound logic that backs them. And in so doing, he leaves us with an alternative interpretation of the historical record that I think can only be properly viewed by letting go of some of our modern hard money dogma.

For example, the amount of gold that existed in, and made it out of antiquity is probably overestimated. So, if anything, there’s likely less than the current estimates of all gold available today. And gold probably carried a much greater value in antiquity than Hard Money typically assumes. Less gold, circulating as a tradable good (not hoarded, not money) at a really high value relative to everything else. Gold’s primary utility was that you could travel to far-away markets with a great amount of tradable wealth in a small package. It was essentially the trade good that was preferred "on the road," not at home in common everyday trade. It was too valuable for that.

The way gold was used, the way it was valued, the reason why we find more silver, copper, and bronze coins buried at the ancient sites, all this and more has been misinterpreted by our hard money teachers because they project modern thoughts onto the ancients in support of their modern policy prescriptions. FOA said "to understand the value of gold, we must remove ourselves from present time thought and think of gold as the Ancients did." Gaining FOA's ancient perspective is helpful in understanding the ultimate moneyness of gold in Freegold.

I went through GT3 again (for probably the fourth time) just to pull a few tastes and give you the flavor of this masterful piece of conceptual dissemination by FOA:

Gold, that wonderful metal that has all the unique qualities to function as our one and only wealth medium, and we just can't use it without altering its purpose. You know, the Lydians had it right, back around 430 BC. They didn't struggle with the concepts of money, like we do today. They just stamped whatever pieces of gold they found laying around and kept it for trade. There was no need to clarify for certain that their gold money needed properties of "utility", store of value, medium of exchange, etc. etc.. They didn't need to identify these qualities were in gold before they stopped questioning if it was safe to use gold as savings. Gold was owned and the knowledge that people owned it and carried it for trade was alone enough to make it "worth its weight as wealth".

You see, back in antiquity there existed another property that could override our need for modern definitions of tradable wealth. That property was found in the one identifying mark of wealth that transcended all ages; real possession!(smile) This factor and this one factor alone had the ability to activate all the other modern attributes of money properties, even when the knowledge of these attributes was unknown in the ancient era. Come now, Alexander the Great didn't know about "utility" did he? (grin)

--------------

Wealth.

As a means of example; think about art work for a moment? That fine painting that graces your main prominent wall. It's tradable for something, isn't it? Perhaps that Renoir for the acreage down the street. That use would cover some of the medium angle, right? A little bulky, but the large value makes it no more or less cumbersome than five gold bricks.(smile) Utility? Just watch your friends stare at it for hours. Store of value? A Renoir? We don't even need to discuss this.

But, one more thing, is it wealth? Of course it is. You see, it is wealth because you possess it, and the very knowledge that you possess it is held by others.

These paintings command a value, a price, a demand, precisely because every one of them is possessed by an owner. In the world of wealth, worth is enhanced because the supply is lessened by this "possession attribute". And possession is how most people in antiquity understood wealth.

++++++++++++++

Many hard money philosophers have pointed their finger at others for the fiat situation we use today. It was the bankers and governments, the kings and cohorts, big business and robber barons or some communist manifesto that forced us to use this type of money. Well, you may not like the process and consider yourself above or apart from it all. You may even declare all of them evil. But, in the end, one fact remains; society may govern itself in many ways over thousands of years, but it has never stopped the evolution that corrupts the use of real money as official money.

Over time and life spans gold has been brought into official use countless times. Only to be bastardized by forces, we as peoples can never control. After every failure and ruination of much wealth, the cries always return to bring gold back as money. Once again to begin the long hard road that leads to the same conclusion. Gold coins, then bank storage, then gold lending, then gold certificate use, then lending of certificates, then certificates are declared paper money, then overprinted, then gold backing removed, then price inflation, then,,,,,, we begin again. But this time it's different the hard money crowd say. Yes, it is. Only the time has changed.

For the better part of human existence, gold alone has served all of the best functions of tradable wealth. But as soon as we call it our money, human nature takes over. Yes, we can call it a stock or a bond, a piece of land or a painting, a car, boat or antique, but just don't label it as money.

++++++++++++++

Going back over #56 "The Gold of Troy":

You noticed that I structured that discussion in a way that makes the independent mind wander about. Let's pull those thoughts together and move along.

We found that history had left us with some conclusions that were, it seems, never concluded. Archaeology had never been approached by someone like us, with a different hard money perspective. Yes, all the records were there, but most every paper written on the subject appeared carbon copy. They all projected our modern sense of money into the economic structures as they existed back then. "Of course, we are today more complicated", our history papers said,,,, so,,,,,, allowing for that difference "the ancients still operated back then the same as us now". How neat!

Yes, our teachers "called our perception of money, their money and our perception of goods, their goods" in the same context we can use now. They said "hey, they were using hard money to buy and sell from each other, just like we once did" Again,,,,, how neat"!

++++++++++++++

For us, as hard money "Physical Gold Advocates", to understand the value of gold, we must remove ourselves from present time thought and think of gold as the Ancients did. Not as money but as little tradable hunks of metal. Gold for goods, straight up, as the citizens of Troy did!

It's the Physical Gold Advocate's "advantage", because while he is waiting for the real value to emerge, the real value that we know existed in antiquity has never gone away! It just doesn't have a marketplace to show it. It will.

I use the phrase; "our advantage of owning the metal", because buying physical gold for today's currency,,,,,,, is like buying a lifetime wealth option that never expires. The commission one pays for this gold coin position, in the form of what we call today's price,,,,,,, may one day go to almost zero as our paper market structure fails from the discovery of real price.

++++++++++++++

So, with the Athens, Macedon, Tarentum and Antiochus to name a few, began the world's first coins. Gold coins? Yes they were, but money as we know it? Our view of how these people viewed and used this gold money is, we believe, far different from what gold scholars teach. And its impact on estimates of existing modern gold supply and use is enormous.

All throughout these early times, prior to BC and into some AD, people didn't see these gold coins as we think of money today. These various gold coins had tremendous value, but they were just gold pieces. They were wealth for trade like everything else was. That's simple logic, I know, but the vessel of oil, for instance was just as tradable as a gold coin. In fact, within most of the medium sized city states of that era, barter of like goods was just as good or better than gold coin. One's life was better if he owned wealth he used.

++++++++++++++

More to the point, this logic made these guys spenders of gold, rather than savers! If you had gained gold in trade, for your services or goods supplied, you had no reason to save it. There was no other money that needed to be hedged against value loss.

It's becoming more and more apparent that average people of that time quickly traded (spent) their gold for something useful of value, for both them and their family. They didn't have the excess we know today. In modern nomenclature; this logic dictates that a much smaller amount of gold money circulated and circulated faster than many supposed.

For longer savings, even for those of above average means that had all they wanted, people tended to spend their most valuable gold coins first, while saving the least valuable (bronze, silver, iron) for emergencies and later use. To us, today this sounds strange, but place yourself in that time. It was better to build your most useful and needed store of things while times were good.

Therefore, you traded the gold, which brought the most equal trade, first. If things got so bad that one had to dig up the stash, you were trading for last ditch things anyway. Kind of like wrapping up and burying beef jerky to get you thru a pinch. This use of lower metal is supported. Remember, lots of things served as money objects then. Even much later, AD, it was common in Rome to trade big iron bricks that were forged as a bull. Its use was in trade for "one bull" or something of that animal's value.

++++++++++++++

When evaluating lifestyle wealth, back then, many often find themselves comparing things in a relative mode with today's perspective. In this position we think the mark has been far missed for gold worth. It's possible that gold payment, in these early times amounted to a huge premium compared to today. The various goods and lifestyle conditions in existence indicate a much higher relative worth for their goods of daily life. Thereby giving gold a much greater relative worth within one's life also. If a one stater Darius of gold, from Cyrus of Persia was worth a very valuable vessel of oil, why utilize the effort to find gold just to trade for some oil. Better to skip the gold production and make the oil. This was the norm for thinking by people not trading on the road, living "within local" city states. Indeed, outside the need to pay armies, a much smaller amount of gold did the job much better than us modern thinkers thought was necessary. Further, the use of oversea warfare and trade perhaps lost more gold into the ocean than we will ever know.

Consider these possibilities well. In that gold today is in a much lesser existence, compared to modern goods supply and lifestyle enhancements, when comparing it to its value in life in the past. It's true worth as a wealth medium could be a 1,000 times higher! For it to return to its ancient position of true asset wealth, for trade outside the modern currency realm, we can see where its European benefactors have once again placed it "On The Road" to much higher fiat currency prices.

++++++++++++++

Back then, there was no other currency. No paper moneys or banks. One had no need to save gold as a hedge or savings account. Your wealth was in the useful things contained in the world around you. Those little hunks of metal were just that, little hunks of gold that everyone knew had trading value. They were not money, not the way we think of money today. They were just a beautiful metal, gold.

++++++++++++++

The Lydians, Greeks and Romans all held gold. From Parthia through Rome and on to the Visgoths, Lombards, Normans and Franks, they all held gold as wealth. It was wealth first and traded as what we call money second. Possession identified that gold as real wealth, even if that ownership was for but the moment of a trade.

From the earliest times right into the Old World periods of Europe, gold served as the most valued wealth asset one could use in trade. It was by far the largest unit of tradable wealth in circulation that could be counted on to bring a premium in trade while shopping between cities. It moved, it flowed and it traveled. It was indeed, always "on the road"! Lesser metals and other tradable wealth assets always competed with gold for its trading function, but only gold made the best "on sight" trade. When given the choice of other "almost moneys", gold would always bring an extra slice of meat or fuller basket of cloth.

The irony of gold use over most of its earlier periods was that few average people kept it for long. Hence the seldom discovery of gold coinage where average people lived (see my earlier posts). To be sure, it represented wealth to these commoners, in good form and to the highest degree. Yet, their possession of this wealth usually constituted only a short time period. This short ownership occurred because gold did, would and could trade so much better for the needed things in life. For the worker, service wages paid in gold meant you just got a bonus or raise and the time had come to finally buy what you couldn't afford if paid in other means. If these people saved at all, it was usually in the form of the lesser metals (see my other posts).

---------------

If gold was so valuable back then, there must have been a bunch of it saved and transported into our modern time?

No, not really! We used to try and extrapolate all the gold that was mined and turned into jewelry, bullion or coin. If it was so good for coin and trade, civilizations must have saved every ounce, we thought! But something kept nagging at our conclusions. Something that kept turning up over and over at our digs.

Some of you have seen the Gold of Troy pieces or other fine examples of old gold craftsmanship at other museums. Ever notice how good they were at making gold so long ago? From intricate bracelets to rings, head dress items to fine cups, even the most thin of leaf. Some of it was so small we had to use magnifying glasses to see the work clearly.

This gold in jewelry and art work form was the other major form of traveling wealth. In many of our recent findings we now think that jewelry and coin traded places as easily as getting your check cashed today. Throughout the ancient land, gold centers occupied the trade routes. Any gold that rested for too long was quickly recruited into a form that worked for the next traveler. In fact, evidence now points to all forms of gold ownership, not just coins, being a short term proposition for the average man. Indeed, contrary to what we thought, the fingers of all mankind did, through the ages, touch gold!

Now place yourself in that time. You work for Rome in the army, a fighting man. Not all of you were paid in lesser metals, many of you were relatively better off. You did carry some of your wealth with you in the form of gold coin or jewelry. In the case of a Roman soldier, a gold ring was very probable. When you went into battle, did you leave your few gold items laying in the tent? Or did you wire them back to a Swiss bank for safekeeping until after the battle? (big grin)

What we are finding, in the form of molecular fragments at battle sites, leads us to believe that most wars were fought with most wealth possessions worn or in pockets. Gold included. To make a long story short, we now believe that a great deal of early gold was scattered on trails, in the sea and during every war. In fact, rubbed, scraped and powdered to the four winds.

Because gold was so valuable in long trade, extremely small creations were carried as jewelry. Much smaller and much more able to be lost than other larger units of the lesser metals. The nature of so much of this gold was that it was easy to be lost and dispersed. Especially considering the modes of travel back then. We as museum visitors see all the magnificent pieces displayed. What we don't see are the countless broken, partial and fragmented items that are never offered for viewing.

Knowing what we know now, we believe that a very large portion of gold was lost and scattered on a yearly basis. Add to this the fact that most gold mining brought almost the same return as making many of the goods it purchased and we can see how gold was and is over counted. Where it was once taken as fact that all gold was looted and remelted, we now think that gold stocks were lucky if replaced.

By the time of the great gold coinages in Europe, the gold that flowed into these major commerce centers was all there was left in the world!

++++++++++++++

The real issue is our misunderstanding and misuse of the term "sound money". That thought has been bantered around for hundreds of years. Truly it does not exist except in the minds of men.

Money, the term, the idea, perhaps the ideal,,,,,,, is something we dreamed up to apply to one of our chosen units of tradable wealth. Usually gold. We could take almost every item in the world and use it in this same "money fashion". Still, this form of trading real for real is just exchanging wealth. It isn't exchanging money as we understand money.

Gold is no different than anything else you possess as your wealth, it just so happened to be the most perfect type of tradable wealth in the world. So it evolved to be used the most and eventually labeled in the same function of what we consider to be "sound money".

Now, consider that all wealth is represented in and of itself. You cannot reproduce wealth through substitution, like giving someone five pieces of copper for one piece of gold and then have them think they now have five pieces of gold! This is the process we try to perform within the realm of man's money ideals. We have always debased trading wealth by duplicating it into other forms and calling all of it, collectively, "our money".

This duplicating, this replicating, this debasement is the result of taking the concept of a credit / contract function (paying in the future) and combining it with the concept of completing a trade at the moment. Think about that for a moment?

As an example, I'll give you a paper contract to pay you later for some oranges and you give me the basket of oranges. Better said, I just gave you modern man's actual concept of money.

Or I trade you a basket of apples "or gold" for those same oranges and the deal is finished, done! We have been taught to think that this is also the concept of money trade.

The first uses what our currency system has evolved into, what is really money in our mind. Where the second uses no credit form at all and is more comparable to trading real wealth as the ancients traded using gold.

Contemporary thought has always blurred these two notions; saying that these two methods of trading are one in the same and both forms use the same idea of what we think money is.

++++++++++++++

This is the road ahead. A fiat no different from the dollar in function, yet a universe away in management. A wealth asset that also stands beside this money, yet has no modern label or official connection as money. In this way modern society can circle the earth, to once again begin where we started. Having learned that the concepts of wealth-money and man's money were never the same.

++++++++++++++

They are not trying to Un-money gold! They are going to un-Westernize gold so it performs its historic function of acting as a tradable wealth holding. No longer following the Gold Bugs' view that governments need to control gold so it acts like real money in the fiat sense. Truly, the BIS and ECB are today "Walking In The Footsteps Of Giants"!

++++++++++++++

Gold will no longer be able to successfully carry the Western name of Money so as to allow for its political price fixing. A process that, it seems, has been with us for generations. Enslaving millions of hard workers by always officially classifying the terms and value of both their paper currency and their metal savings. Always inflating both items for the good of society's never ending political agenda.

Allowing FreeGold to circulate as a wealth asset would denominate its true worth through the much larger real demand of "Wealth Possession" instead of paper possession. Such a gold scale would measure our world reserve currencies against each other instead of against our Western concept of gold as official money. But, in addition, on a higher level, prevent any one country from subjugating other nation states through fiat dominance. To more fully grasp the impact of "Possession" and why ancient gold was worth so much more as FreeGold; hike again that part of our trail (FOA (04/18/01; 20:20:06MT - usagold.com msg#64) Lombards, Normans and Franks.)

++++++++++++++

We were first alerted to the "gold is money" flaw years ago. When considering the many references to gold being money, in ancient texts, several things stood out. We began to suspect that those translations were somewhat slanted. I saw many areas, in old text, where gold was actually more in a context of; his money was in account of gold or; the money account was gold or; traded his money in gold. The more one searches the more one finds that in ancient times gold was simply one item that could account for your money values. To expand the reality of the thought; everything we trade is in account of associated money values; nothing we trade is money!

The original actual term of money was often in a different concept. In those times barter, and their crude accounts of the same, were marked down or remembered as so many pots, furs, corn, tools traded. Gold became the best accepted tradable wealth of the lot and soon many accountings used gold more than other items to denominate those trades. Still, money was the account, the rating system for value, the worth association in your head. Gold, itself, became the main wealth object used in that bookkeeping.

This all worked well for hundreds and perhaps thousands of years as fiat was never so well used or considered. Over time, society became accustomed to speaking of gold in the context of money accounting. Translations became all the more relaxed as gold and money accounting terms were mingled as one in the same. It was a subtle difference, then, but has become a major conflict in the money affairs of modern mankind; as gold receipts became fiat gold and bankers combined fiat money accounting with gold backing.

++++++++++++++

To understand gold we must understand money in its purest form; apart from its manmade convoluted function of being something you save. Money in its purest form is a mental association of values in trade; a concept in memory not a real item. In proper vernacular; a 1930s style US gold coin was stamped in the act of applying the money concept to a real piece of tradable wealth. Not the best way to use gold, considering our human nature.

++++++++++++++

By accepting and using dollars today, that have no inherent form of value, we are reverting to simple barter by value association. Assigning value to dollar units that can only have a worth in what we can complete a trade for. In effect, refining modern man's sophisticated money thoughts back into the plain money concept as it first began; a value stored in your head! Sound like something that's way over your head of understanding? I'll let you teach yourself.

++++++++++++++

You use the currency as a unit to value associate the worth of everything. Not far from rating everything between a value of one to ten; only our currency numbers are infinite. Now, those numbers between one and ten have no value, do they? That's right, the value is in your association abilities. This is the money concept, my friends.

++++++++++++++

A fiat trading unit works today because we make it take on the associated value of what we trade it for; it becomes the very money concept that always resided in our brains from the beginnings of time. In this, a controlled fiat unit works as a trading medium; even as it fails miserably as a retainer of wealth the bankers and lenders so want it to be.

++++++++++++++

For thirty years fiat use evolved on its own to embrace the non-wealth trading aspects of "the money concept". Leaving in its wake a world of worthless dollar debt as people bought wealth outside the "money concept" anyway. We are, today, in a transition away from that dollar mess and much of our wealth illusion will be passing from our grasp in the process.

In every way, society is trading its way back to where it started. In the process, gold will find a new value from its history in the past:

"A wealth of ages savings for your future of today."

End Sidebar

_________________________________________________________

Well, there you have it! The pure concept of money is our shared use of some thing as a reference point for expressing the relative value of all other things. Money is the referencing of the thing, not the thing itself. As FOA said, money is "a value stored in your head!" Money is not something you save. "Money in its purest form is a mental association of values in trade; a concept in memory not a real item… the value is in your association abilities. This is the money concept, my friends."

But what does this have to do with me in 2011? I can almost hear you thinking this question now. Well, I'm going to share a secret with you. The big secret is that the people's money is simply credit. And by "the people's money," I mean our money, the real producing economy's money. The monetary base is only the banks' and governments' money, except for that little bit of cash you keep in your wallet for emergencies. Let me explain.

Today's monetary base is a clearly defined thing. It is all physical currency plus reserves held at the Fed. We the people cannot have electronic base money. We cannot open an account at the Fed. Only banks and the government can. We use commercial bank credit and private credit to keep the economy churning. The reference point of our credit is the base. We reference that base when we transact in "dollars".

Private and commercial bank credit appears and disappears spontaneously all the time, all throughout the real economy. This is what actually lubricates the economic engine; having a base of stable value to which we refer in monetary transactions. Private credit is generally cleared using bank credit. And bank credit is cleared using the monetary base. But all credit denominated in dollars refers to that base and relies on a stable unit value or price stability.

It is the banks' job (both commercial and central banks) to make sure that bank credit (the people's money) and base money (the banks' money) are fungible. That is, they are always freely and equally exchangeable. But of course they are two separate things, credit and base money, with two very different volumes. Under normal conditions, there's a lot more credit money floating around than there is base money. So keeping them fungible can be a juggling act on occasion. But for the most part, we the people choose to hold bank credit as our money rather than cash. And, in fact, it is the limited availability of cash in the system (its relative "hardness") that keeps our money stable in unit value.

Think about it this way: We are free to choose cash at any time. And when we go to the bank to exchange our credits for cash, we put that bank under pressure to come up with cash that is relatively "harder" to come up with (more limited in volume) than credit. Let's say, for example, that "demand deposits" (those that can demand cash on the spot) are ten times larger than the total volume of cash in the system. Is this good for our money? Yes, because it means that the reference point unit we use is in limited supply, which keeps a vital tension on the overall system. The operations the bank must do to come up with our cash (sell off some value) maintain value in our credits.

Say the base volume is one trillion dollars, which is about what it was in October of 2008. That means the base unit reference point for all dollar credit in the world is one one-trillionth of the base volume, all the available above-ground dollars ever mined throughout all of history. Then imagine you doubled that base to two trillion dollars. The unit reference point will have been cut in half, from one one-trillionth to one-half of one one-trillionth of the base volume.

Say you've got a contract or a credit for a kilo of gold. Now obviously the total volume of gold can't be doubled overnight like the dollar base was, so what would be the equivalent effect? Well, it would be like someone cutting that reference kilo in half. Your one kilo contract, since it is denominated in kilos, refers to this unit reference point that has just been cut in half. It has suddenly become twice as easy for your creditor to deliver on his obligation. And, by the way, the volume of the dollar base has more than doubled since Oct. 2008. It's now at 2.7 trillion, which means the unit reference point was actually given a 63% "haircut" in three years, from one one-trillionth to little more than one-third of one-trillionth of the total volume.

Now, before you start arguing your own favorite economic pet theory, let me remind you that there is no right or wrong at this point. There's only the usefulness of a perspective in delivering the correct analysis of what's actually happening today and the best prescription for your personal action. But you can't use a perspective until you get it. Then, and only then, you can use your own mind to decide if it is the correct perspective and then act upon it. Later it will be proved correct or incorrect, just as Another said: "time will prove all things."

Clearly the 63% destruction of the dollar unit reference point over the last three years did not immediately translate into a 170% rise in prices at the grocery store. And I wouldn't expect it to. It never works like that. Henry Hazlitt explained it like this: "The value of the monetary unit, at the beginning of an inflation, commonly does not fall by as much as the increase in the quantity of money, whereas, in the late stage of inflation, the value of the monetary unit falls much faster than the increase in the quantity of money."

If you have a large 401K, IRA or pension fund full of credits for dollars, you may be taking comfort in the fact that the 63% haircut in the very unit your retirement nest egg references has not yet shown up at the stores where you shop. But the fact remains that the dollar has been debased. That's why they call it debasement. The base is diluted by expanding its volume which reduces the value of the unit used for reference relative to the volume of available units.

There are, of course, plenty of economic theories out there that are wholly designed to distract your attention away from this plain and obvious debasement and to tell you why it doesn't matter, and how the presently slow price inflation is proof that it doesn't matter if they debase your money and your life's savings. Some will tell you that the apparent fungibility of credit and cash means they are the same thing. And some will even try to tell you that the base unit reference point derives its value from the volume of credit rather than its own volume, and that the base volume is essentially meaningless. But I think that if you are keeping your wealth in the form of money, sheep being periodically sheared is an image worth keeping in mind.

The Pure Concept of Wealth

Another concept of concern today is that of 'wealth'. As FOA emphasized in the sidebar, the fundamental property of wealth is that of "possession." It is by this property that wealth is identified, and thereby it becomes 'wealth'. "In the world of wealth, worth is enhanced because the supply is lessened by this 'possession attribute'. And possession is how most people in antiquity understood wealth."

Have you ever noticed how the super-rich seem to stay super-rich no matter how much money they spend? Not only that, but they seem to get wealthier the more they spend! They buy amazing super-homes, expensive antique furniture to fill the homes, and priceless artwork to hang on every inch of their fancy walls, yet somehow they retain their wealth.

That's not to say that they don't also participate in the Western tradition of "the something for nothing game" we call the paper markets. They do, but that participation does not constitute their 'wealth'. Yet we, the commoners, are told constantly, by state-approved financial advisors, to put our entire nest egg at risk in this "something for nothing game."

We can't afford that nice furniture and art that the super-wealthy buy, so we buy low-priced crap from China that is worth half what we paid for it the minute we walk out of the store. What is going on? Is it possible to imagine a new monetary system that would put common people on equal footing with the super-rich when it comes to possessing our wealth?

FOA (05/06/01; 20:30:52MT - usagold.com msg#69) A Tree in the Making

In this world we all need much; blessings from above,,,,, family,,,, home,,, friends and good health. But after all that, one must have currency and an enduring, tradable wealth asset that places our footing in life on equal ground with the giants around us,,,,,, gold! Understanding the events that got us here and how they will unfold before us is what this GoldTrail is all about.

I know I keep repeating myself, but this post is specifically designed to encourage independent thought; to let your mind wander about, freed from the confines of modern dogma. If you were able to wrap your mind around the pure concept of money, you may be starting to sense the danger, at least conceptually, in holding your lifetime's-worth of accumulated wealth as money. Because when they double the base, they are diluting all of “our” money by half, even if “our money” outnumbers the base by 10:1 (bank credit), 100:1 (all credit), 1,000:1 (credit derivatives) or whatever. It is credit's reference point they are abusing to ease their own discomfort, and our money they are debasing. And the more money you are holding when they do this, the greater your share of the loss.

To contrast these two important concepts, money and wealth, notice that, conceptually, money is not the item that is referenced, and the item (e.g., a dollar bill) is not money in and of itself. It only obtains moneyness by the fact that it is referenced in valuing other items. True wealth, on the other hand, is, in fact, the item itself. A wealth item is wealth, in and of itself, by the mere fact that it is possessed.

The easy money camp always wants the savers to store their wealth in money, so they can loot those savings by debasing the referenced unit which eases their discomfort. Meanwhile the hard money camp always wants the debtors' deficit spending to be denominated in real wealth. The problems with this approach are myriad.

So here’s an interesting question: What do you call a monetary system where physical gold wealth (not credits denominated in ounces issued by a commercial bank, but the actual physical stuff) sits on Line 1 of the Eurosystem’s monetary assets? There’s no silver there on line 2, no copper, no oil, no GLD or PHYS, no mining shares, no antique furniture or Renoirs, just 400-ounce bars of physical gold bullion and a few minted gold coins. Official purchases and sales of gold (changes in the volume) are publicly reported every week, and its value is updated every quarter.

What do you call that system? And what do you call the gold in that system? How would you describe gold's moneyness in such a system? And why hasn’t Greece sold its gold yet to end the discomfort? Why do we mainly hear politicians proclaiming "the euro will survive." Why do we rarely if ever see the central bankers sweating "the survival of the euro"? Aren’t they worried about the survival of their reference unit? Or do they simply understand moneyness better than the rest of us?

MMT

If you read my whole sidebar like I hope you did, you saw where FOA described in the broadest terms how we arrived at our latest iteration of easy money. Here it is again:

Gold coins, then bank storage, then gold lending, then gold certificate use, then lending of certificates, then certificates are declared paper money, then overprinted, then gold backing removed…

How's that for covering a lot of years in one sentence?

Depending on which camp you're in, as long as you haven't grasped the pure concepts of 'money' and 'wealth', there's a whole spectrum of descriptions of how "modern money" works with varying degrees of uselessness in practical applicability, both macro and micro. On the hard money side, you'll find lots of criticism of "fractional reserve banking," "thin air money," "borrowed into existence," "credit money is a pyramid scheme" (it's not, the concept of money has always been a credit reference to a base unit), etc., etc… Hard money descriptions of modern money are overwhelmingly critical because, of course, the easy money camp has been in charge for a long time now.

Obviously I think the hard money camp misses the mark in its policy prescriptions, but you've got to understand that they can only address today's issues in the counterfactual subjunctive. In other words, "if A had been true, then B wouldn't have happened or the outcome would have been better." But A isn't true. A being "if only we had hard money today."

But it's over there in the far corners of the easy money camp where you'll find some truly repulsive arrogance by those who unfortunately have the luxury of using true antecedents in their modal logic. Like this: "If it is true today that USG deficit spending is not technically constrained by taxes and borrowing because it issues its own currency, then structural trade deficits are not only sustainable, good and loved by our trading partners, but necessary. 'Austerity', or producing more than we consume at times like these, on the other hand, is a total disaster." That's the logic. Here's the arrogance:

"As a current account deficit nation, the US government can appropriately be thought of as a net currency exporter. This means that we send pieces of paper over to the foreign nations in exchange for goods and services." (Cullen Roche)

"We don’t need China to buy our bonds in order to spend. China gets pieces of paper with old dead white men on them in exchange for real goods and services." (Cullen Roche)

And why doesn’t China just buy other American stuff?

"They have attempted to use their dollars to purchase other USD denominated assets, but the US government has squashed those efforts. So, instead of leaving these pieces of paper to collect dust in vaults, they open what is the equivalent of a savings account with the US government." (Cullen Roche)

"Anyone who uses the term [monetization] in the context of the Fed’s contribution of government spending does not understand how the modern monetary system works." (Cullen Roche)

"This is basic macroeconomics and the debt-deficit-hyperinflation hyperventilating neo-liberal terrorists seem unable to grasp it." (Bill Mitchell)

"The Fed is not printing money. They are merely swapping treasuries for deposits." (Cullen Roche)

Someone should explain to these guys the meaning of the phrase, "never look a gift horse in the mouth." It means that when someone gives you a free horse, you shouldn't inspect it too closely in front of the giver.

Of course this is MMT, or Modern Monetary Theory I'm talking about. Even Paul Krugman noted the arrogance of these theorists in his latest blog post about MMT (my emphasis):

"First of all, yes, I have read various MMT manifestos — this one is fairly clear as they go. I do dislike the style — the claims that fundamental principles of logic lead to a worldview that only fools would fail to understand…"

I bring up MMT not because it is entertaining to make fun of their misguided (and often repulsive) arrogance, but because of the inauspicious rise of their extreme easy money theories right at the tail end of history's grandest easy money experiment. I find it to be a handy platform from which to explain how the ancient concepts of money and wealth are still more relevant to the near-term outcome than a few accounting identities that thrive solely in the monetary plane, and do so with reckless disregard for the real power of the physical plane.

One of the main tenets of MMT is the accounting identity that roughly states the amount the USG deficit spends (government spending in excess of the taxes it takes in) is always equal to private sector net savings plus the trade deficit (exports minus imports, or stated another way, our trading partners' net dollar savings).

This is generally explained with the analogy that the USG spends money into existence and taxes money out of existence. So if the USG (God forbid) taxed as much as it spent (or spent as little as it taxed), there wouldn't be any extra USG money for us mere mortals to save. So by spending more than it takes in, the USG is graciously giving us money for savings. And then, the USG issues Treasuries in an amount equal to that deficit spending (extra money for us to save Woo hoo!) to give us an interest-bearing exchange for our net-production.

To be fair, MMT consistently reminds us it is only describing and not prescribing a monetary system. Fair enough. But the presence of the trade deficit and our trading partners' presumed need for dollar savings should probably set off your alarm bells. If so, MMT wants to calm your worry with these soothing words:

"In a world with global trade we are certain to have trade deficit and trade surplus nations." (Cullen Roche)

In other words, we are simply a trade deficit nation. That's just who we are. Get used to it, and then embrace it! After all, it's pretty cool to get free stuff:

"…the US government can appropriately be thought of as a net currency exporter. This means that we send pieces of paper over to the foreign nations in exchange for goods and services." (Cullen Roche)

It's pretty neat the way accounting identities work. They are always true because, by definition, they must be true. They are like saying, "the amount of widgets sold equals the amount of widgets bought." You can't really dispute them as they are framed. But it is in the static assumptions that go into the careful monetary plane framing that flaws can be found. The physical plane can be much more dynamic than they assume.

For example, what if all the private sector net-producers decided to save in gold instead of USG debt? Since the accounting identity we're talking about includes our foreign trading partners like China, I'm essentially asking what happens if they (and we) stop buying Treasuries. Remember that Cullen says it doesn't matter:

"We don’t need China to buy our bonds in order to spend. China gets pieces of paper with old dead white men on them in exchange for real goods and services." (Cullen Roche)

In other words, if they don't buy our Treasuries (run a capital account deficit), then they'll just stack the Benjamins. In other words, that's just the way it is. See? It's an accounting identity.

But then a reasonable person might point out that the USG still issues Treasuries equal in amount to all its deficit spending. And if we and the Chinese aren't buying them, then the Fed has to, so it makes up a cool name like QE2 to disguise the real purpose of the purchases. Not so fast, MMT says. The Treasury does not need to issue debt in order fund its spending. When it spends, it simply credits private sector accounts with new credit money and the banks with new base money. There is no direct connection between sales of Treasuries and money spent other than a myth in our confused minds.

In fact, during the debt ceiling debate in late 2009, MMT actually advised them to stop issuing Treasuries and just keep spending:

"The anti-deficit mania in Washington is getting crazier by the day. So here is what I propose: let’s support Senator Bayh’s proposal to 'just say no' to raising the debt ceiling. Once the federal debt reaches $12.1 trillion, the Treasury would be prohibited from selling any more bonds. Treasury would continue to spend by crediting bank accounts of recipients, and reserve accounts of their banks. Banks would offer excess reserves in overnight markets, but would find no takers—hence would have to be content holding reserves and earning whatever rate the Fed wants to pay. But as Chairman Bernanke told Congress, this is no problem because the Fed spends simply by crediting bank accounts.

This would allow Senator Bayh and other deficit warriors to stop worrying about Treasury debt and move on to something important like the loss of millions of jobs." (L. Randall Wray)

I want you to notice a small detail in the above quote that probably slips by most people. Wray writes (my emphasis): "Treasury would continue to spend by crediting bank accounts of recipients, and reserve accounts of their banks."

Out here in the real world of the productive economy, when we spend, only the account of the recipient gets credited. Not the reserve account of their bank. The "reserve account of their bank" is that commercial bank's account at the Federal Reserve Bank. Remember? You and I can't have accounts there. Only the banks and the government can. Our spending is netted out in the system each night and the imbalances between banks are cleared with those substantially smaller reserve accounts.

I imagine there's a good reason Randall Wray was careful to include this small technicality in his piece. That's because raw government-created money through deficit spending is fundamentally different from "our money." Government spending adds one unit of credit money (our money) to the system as well as one unit of base money (their money). The bank receiving the deposit gets a reference point unit asset to match the liability it takes on.

So the volume of the base is expanded when the government spends, and it is likewise contracted when the government taxes and/or sells Treasuries to the private sector (including our trade partners like China). But when the government spends in excess of those two operations (taxing and debt selling), the base volume is simply expanded. And MMT apparently sees no difference between the true concept of money (all that 100s of trillions of credit denominated in a single reference point unit) and the base which it references. Take QE2 for example.

"Unlike Zimbabwe, which had to have U.S. dollars to pay its debt to the IMF, the U.S. can easily get the currency it needs without being beholden to anyone. It can print the dollars, or borrow from the Fed which prints them.

But wouldn’t that dilute the value of the currency?

No, says Cullen Roche, because swapping dollars for bonds does not change the size of the money supply. A dollar bill and a dollar bond are essentially the same thing."

This is part of the flaw in MMT’s view. Bonds are credit (the economy’s money) denominated in (referencing) the base unit (the dollar). Swapping credit for base units dilutes and debases every single credit dollar in the world, all quadrillion of them if you included derivatives.

When the private sector (plus our foreign free stuff suppliers) buy bonds, the USG is essentially spending credit money rather than expanding the base because "the credit to the reserve account of their banks" that Randall Wray mentioned above is deleted when the private/foreign sector buys a Treasury bond. Spending credit money does not dilute the base and debase the reference unit. But when the people (or banks) that bought those bonds swap them with the Fed for cash, the base is diluted and the reference unit is debased. So Cullen is wrong. A dollar bill and a dollar bond are not essentially the same thing.

Back in June, talking about QE2, I wrote something very similar to what Cullen says. See if you can spot the subtle difference.

Cullen: "There is not 'more firepower' in the market following QE. All that the Fed altered was the duration of the U.S. government’s liabilities. The Fed took on an asset (treasurys) and also accounted for a new liability (the reserves). But this transaction did not change the net financial assets in the system. The point here is that from an operational perspective the Fed is not really altering the money supply."

Me: "The Fed has not created more money, it has simply changed the nature of existing money. Remember, FOA said that '...hyperinflation is the process of saving debt at all costs, even buying it outright for cash.'"

So, just to recap, MMT says that neither selling debt to the Chinese nor QE (selling it to the Fed) is actually necessary to fund government deficit spending. The government spending actually happens first, therefore it is independent of, and not reliant on, either of those financial operations. And to this point, I think we can all agree with MMT's description of the process as it exists in the monetary plane, although it is clearly not the only correct description, and certainly not the whole story.

Here's the thing, the act of government deficit spending without either counterbalancing taxes or Treasury sales to the private/foreign sector, and the act of Fed quantitative easing, both change the nature of the money supply in a way that all other "normal" activities do not. They debase "our money" by expanding "their money" in volume to ease their discomfort. And this kinda gets us to the driving thrust of MMT; that MMT sees little to no danger of this monetary plane debasement spilling out into the physical plane with deadly consequences for the dollar.

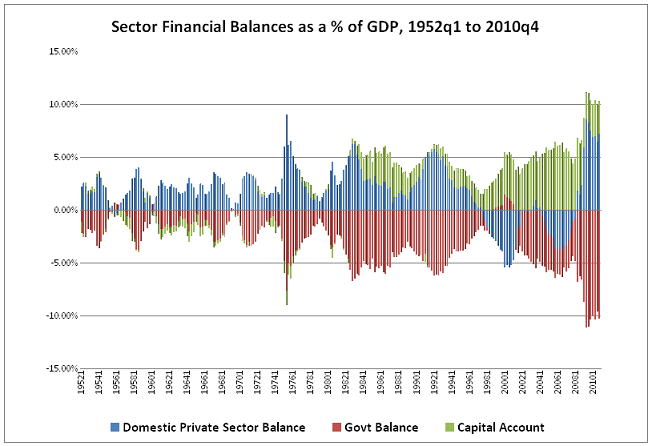

There is, however, one area in which the danger is at its all-time peak today. And that is the US trade deficit as viewed from the physical plane. But before we get into that, let's take a look at a couple neat charts that Cullen Roche uses to visualize the monetary plane accounting identity that underlies his theory. Cullen calls them "sectoral balances," meaning the monetary plane balance sheet of three different sectors: the government sector (USG), the domestic private sector, and the foreign sector.

What I'm going to try to do is to help you see the physical plane reality of these charts. They are so neat and balanced in the monetary plane, yet they represent an immense imbalance in the physical plane that, because of the credibility inflation of the last 40 years, leaves the dollar vulnerable to spontaneous hyperinflation. More on that in a moment.

In this first chart, I want you to pay special attention to the dashed blue line. In the monetary plane, that line represents the amount of US paper our foreign trading partners are taking in each year. When they take in dollars, those show up as a current account surplus on their sheet and a current account deficit on ours. Then when they trade them in for Treasuries they show up as a capital account deficit on their sheet and a capital account surplus on ours. But the easiest way to understand this blue line is in the physical plane. It represents the trade deficit; the amount of free stuff we got each year in exchange for nothing but paper. As Cullen says, "the US government can appropriately be thought of as a net currency exporter." So the blue line is our "currency exports."

Here's a link to our Balance of Payments (BOP) from 1960 through 2010:

The first column is our trade balance. A negative number means a trade deficit. I'm sure the MMT folks reading this are getting tired of me calling it "free stuff," but that's what it is, which I'll explain in more detail later. Foreign central banks were literally supporting our trade deficit for their own reasons for the last 30 years. You'll notice we went into deficit in 1971, with the only blips up into surplus since then occurring in '73 and '75.

You've probably heard it said that the US has become a "service economy" as opposed to producing all the real stuff we used to produce. Well, if you look at the second and third columns, the goods column and the services column, you'll see the inflection point of that transition was also in 1971. So all those negative numbers in the first column really do represent real goods, the kind of stuff that gets packed into containers and physically shipped to the US.

In 2010 you'll see that our trade deficit was $500 billion. That number comes from a $645B deficit in goods, and a $145B surplus in services. In 2011 we are on track for a trade deficit of about $565B (monthly data). For the last decade, our trade deficit range has been $400B - $750B per year. The average for the decade is $581B per year, or $48.5B per month.

Now this second chart really shows the monetary plane symmetry that MMT loves. The whole point of the accounting identity is that the balances of the three sectors (government sector, domestic private sector and foreign sector) must net out to zero. One person's savings is another person's debt, or so the story goes. Remember what I said about widgets? "The amount of widgets sold equals the amount of widgets bought." Well the accounting identity behind this chart is essentially just as simple: "the amount of debt sold equals the amount of debt bought." If you're going to save, then I have to deficit spend (create debt notes) for you to hold as your savings. Neat, huh?

On this chart, the bottom is the amount of debt sold and the top is the amount of debt bought. All that red on the bottom is the government sector selling debt. The green on the top is the foreign sector buying that debt. The blue, which seems to jump around, is the domestic US private sector either buying (top) or selling (bottom) debt (think: MBS). What I want to draw your attention to is this last bit of blue at the end:

What this section, roughly encompassing the last three years, apparently shows is that 1. The debt sold by the USG jumped dramatically, 2. The debt purchased by the foreign sector decreased, and 3. The domestic US private sector apparently picked up the slack dropped by the foreign sector. I propose to you that "the domestic US private sector" in this case was mostly Ben Bernanke and the Federal Reserve. I do understand that MMT interprets QE as something other than money printing, but I would like you to read this paragraph from Wikipedia on the specific amounts of quantitative easing:

"The US Federal Reserve held between $700 billion and $800 billion of Treasury notes on its balance sheet before the recession. In late November 2008, the Fed started buying $600 billion in Mortgage-backed securities (MBS). By March 2009, it held $1.75 trillion of bank debt, MBS, and Treasury notes, and reached a peak of $2.1 trillion in June 2010. Further purchases were halted as the economy had started to improve, but resumed in August 2010 when the Fed decided the economy wasn't growing robustly. After the halt in June holdings started falling naturally as debt matured and were projected to fall to $1.7 trillion by 2012. The Fed's revised goal became to keep holdings at the $2.054 trillion level. To maintain that level, the Fed bought $30 billion in 2–10 year Treasury notes a month. In November 2010, the Fed announced a second round of quantitative easing, or "QE2", buying $600 billion of Treasury securities by the end of the second quarter of 2011." (Wikipedia)

Now, before we move on, I want to draw your attention to three curiosities to which I will be referring:

1. Using the latest data for the last three years, the dollar monetary base expanded by $1.7T and the US trade deficit (free stuff inflow) was $1.5T over the same time period.

2. For fiscal year 2011, the trade deficit was $540B and "QE2" was $600B over the same time period.

3. For the last year, Chinese Treasury holdings are perfectly flat (same amount held in Aug. 2011 as in Aug. 2010) and Hong Kong holdings are down by $26B.

The Debtor and the Junkie

The USG may be a dealer in the monetary plane, but it is most definitely a sketchy junkie in the physical plane. The USG thinks (and truly believes) that the key to rejuvenating the US economy is trashing the dollar as a short cut to increasing exports (reducing the trade deficit). But what it can't see (nor anyone that focuses solely on the monetary plane for adjustment) is that the huge trade deficit the USG wants to quit is actually its own heroin fix. This is a deadly combo for the US dollar.

MMTers don't think very highly of "hyperinflationists". They call us "hyperventilators" and such, although I shouldn't really bunch myself in with the others. I think my description of hyperinflation is more in line with reality than others I've read. See here, here, here, here and here. But in this post I hope to show you where the MMTers go wrong on hyperinflation, and to show why—and how—dollar hyperinflation is the only possible outcome.

The "debtor" I had in mind for my section title was Weimar Germany in the early '20s, not the USG today. The USG is the junkie. Weimar Germany owed war reparations, a debt resulting from WWI that was essentially denominated in gold. This was a debt in a hard currency (hard as in difficult, not hard as in solid), unlike the USG who owes its debt to others in its own currency. MMT got that part right. The USG cannot be forced into involuntary default on its own currency debt. And because of this property, USG debt is a monetary plane illusion when viewed from the physical plane. It is a great store of nominal value, and a terrible store of real value.

Where MMT derails from the description track and goes careening off the prescription cliff, the message is usually about the admirable goal of full employment. You know, the Fed's other mandate. Indeed, L. Randall Wray's book is titled Understanding Modern Money: The Key to Full Employment and Price Stability. But the bottom line is MMT's untested theory that the USG could pay for full employment (hire anyone who wants to work) through raw monetary base expansion while enjoying the same relatively stable prices of the last 30 years. And their best defense of this shark jump proposition appears to be debunking the hyperventilators.

"MMTers are commonly accused of promoting policy that would recreate the experiences of Zimbabwe or Weimar Republic hyperinflations. These were supposedly caused by governments that resorted to “money printing” to finance burgeoning deficits—increasing the money supply at such a rapid pace that inflation accelerated to truly monumental rates." (Wray)

He goes on to explain how the hyperventilators have it all wrong. He shows how hyperinflation is more about an increase in money velocity than volume; that hyperinflation begins with a loss of confidence, not too much money. Any of this sound familiar? Then he beats a gold bug straw man or two before explaining to us how modern money really works. Here's the most important part to understand:

"You cannot print up Dollars in your basement. Government has to keystroke them into existence before you can pay your taxes or buy Treasuries." (Wray)

Notice he mentions taxes and Treasuries. This is important to understand. Government money, which is the monetary base the economy uses as its reference unit, is expanded when the USG spends, and only contracts when you either 1. pay taxes, or 2. buy Treasuries. He wasn't just throwing those out as two examples of how you might spend your money. Those are the only two checks on base money expansion. But the sneaky thing that MMT does is to marginalize the importance of those two methods of contracting the base. Like this, as if it's no big deal, a mere afterthought:

"Usually the treasury then sells bonds to let banks earn higher interest than they receive on reserves." (Wray)